Events

Past Seminars

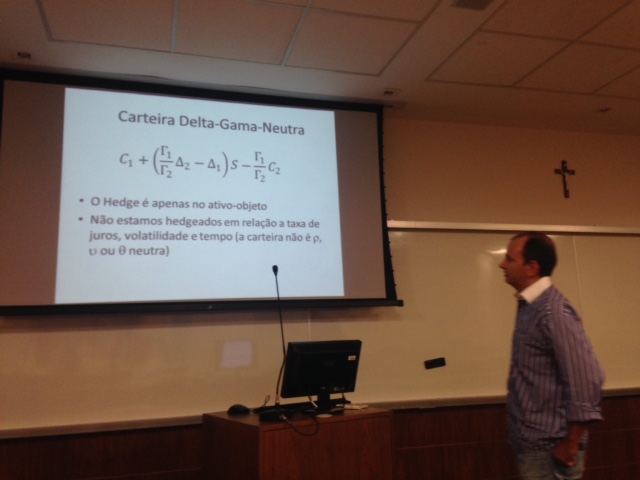

Is the market for option on Petrobras stock efficient? A study based on a Gamma-Delta Neutral strategy

From 13 Apr 2016 until 13 Apr 2016

Wednesday, April 13, 2016 11:00 AM

IAG Business School, Room I-014

Prof.: Gustavo Araújo (BACEN).

Gustavo Araújo has a PhD in Economics from EPGE/FGV, MSc. in Business from IAG/PUC-Rio and a B.S. Production Engineering from PUC-Rio. He is a professor at IAG/PUC-Rio since 2004, at the Department of Economics of IBMEC and in the Master´s program at IMPA. He is an employee of the Department of Studies and Research of the Central Bank of Brazil and one of the authors of the book Derivatives in Brazil – Concepts, Operations and Strategies.

Resumo:

This study aims to determine if the market for options on Petrobras is efficient in the weak form, that is, if indeed public information is reflected in the prices of these assets. For this, an attempt is made to profit systematically through the Gamma-Delta Neutral strategy using the preferred stock of the company and its options. To simulate the strategy as it would be used in the real world, we have built offer books every five minutes considering all buy and sell orders sent to both the underlying asset as for the options. The strategy is realized when we observe distortions between the implied volatility extracted from the options. The results show that the market Petrobras options is not efficient in the weak form, since in 371 operations day trade performed, with an average investment of $81,000 and average time of one hour and thirteen minutes, the average return was 0.49% – which corresponds to 1750% of the CDI in the period – and 85% of strategies were profitable.

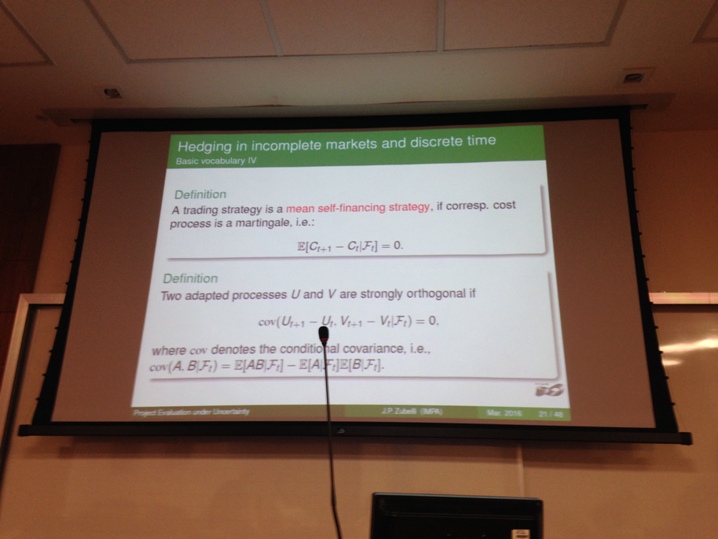

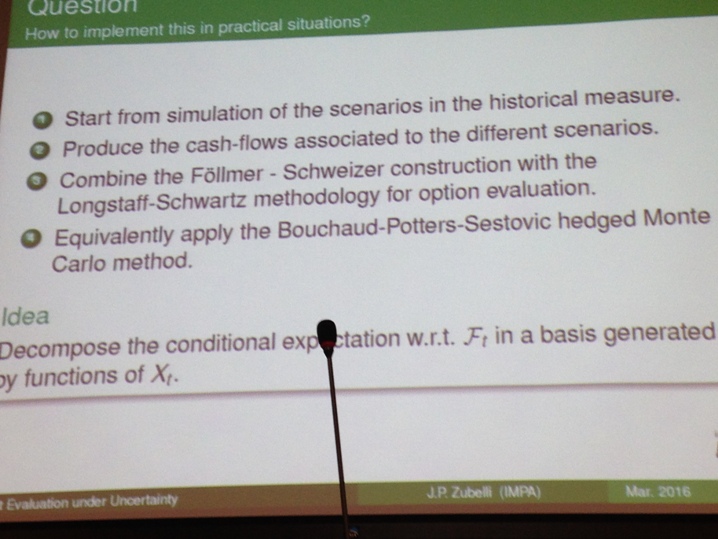

Project Evaluation under Uncertainty: The Hedged Monte Carlo Approach.

From 16 Mar 2016 until 16 Mar 2016

Wednesday, March 16, 2016 11:00 AM

IAG Business School, Room I-014

Prof.: Jorge P. Zubelli (IMPA).

Abstract:

Industrial strategic decisions have evolved tremendously in the last decades towards a higher degree of quantitative analysis. Such decisions require taking into account a large number of uncertain variables and volatile scenarios, much like financial market investments. Furthermore, they can be evaluated by comparing to portfolios of investments in financial assets such as in stocks, derivatives and commodity futures. This revolution led to the development of a new field of managerial science known as Real Options. The use of Real Option techniques incorporates also the value of flexibility and gives a broader view of many business decisions that brings in techniques from quantitative finance and risk management. Such techniques are now part of the decision making process of many corporations and require a substantial amount of mathematical background. Yet, there has been substantial debate concerning the use of risk neutral pricing and hedging arguments to the context of project evaluation. We discuss some alternatives to risk neutral pricing that could be suitable to evaluation of projects in a realistic context with special attention to projects dependent on commodities and non-hedgeable uncertainties. More precisely, we make use of a variant of the hedged Monte-Carlo method of Potters, Bouchaud and Sestovic to tackle strategic decisions.

Downloads

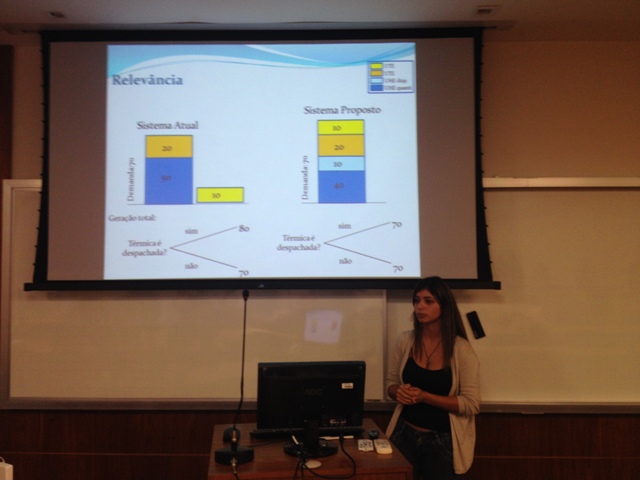

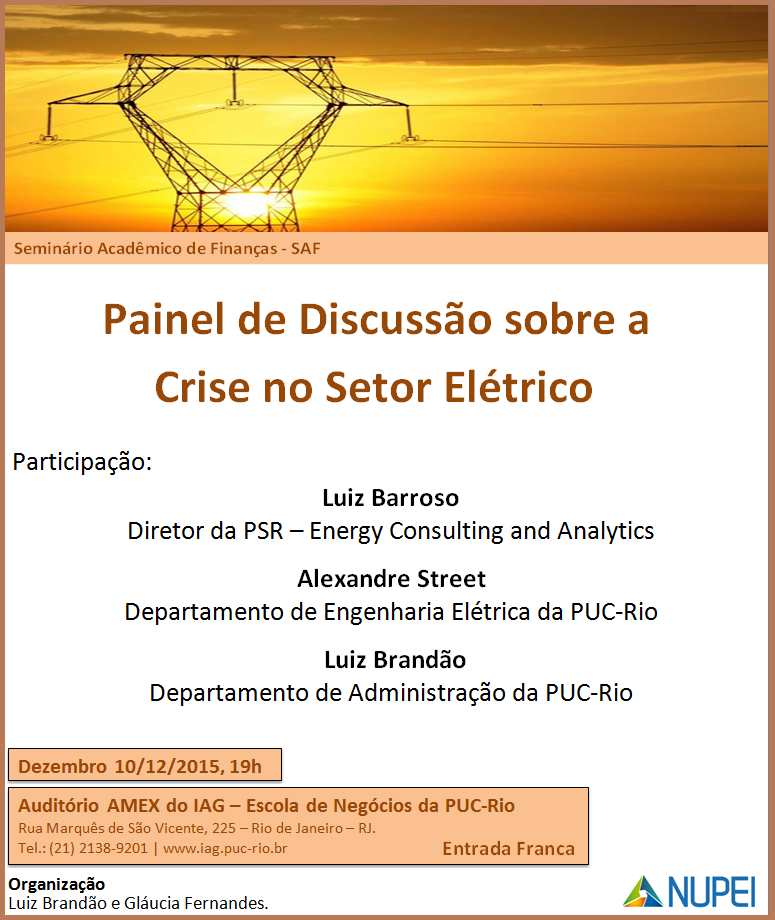

Panel Discussion: The Brazilian Electricity Sector

From 10 Dec 2015 until 10 Dec 2015

Dr. Luiz Barroso – Diretor da PSR – Energy Consulting and Analytics

Dr. Alexandre Street – Prof. Departament of Electrical Engineering, PUC-Rio

Dr. Luiz Brandao – Prof. IAG;PUC-Rio – Moderator

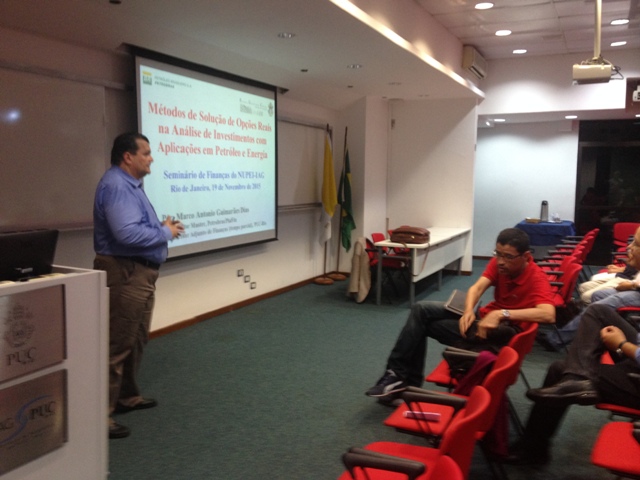

Real Options Theory and application in Oil & Gas

From 19 Nov 2015 until 19 Nov 2015

Dr. Marco Antonio Dias

PhD. Petrobrás and PUC-Rio